The SVN Southwest Region Quarterly Newsletter will keep you informed and equipped with the latest trends, opportunities, and expert analysis in this thriving region. Our team of experienced professionals understands the dynamic nature of the Southwest’s commercial real estate landscape. We are committed to delivering valuable content, including market indicators, investment opportunities, regulatory updates, and localized insights.

The Southwest’s commercial real estate market is recalibrating after years of aggressive growth. Across major metros like Phoenix, San Diego, Denver, and Houston, developers are slowing down as elevated vacancies meet a more cautious tenant base. Industrial continues to be a standout—though vacancy has risen due to heavy deliveries in markets like Las Vegas and San Antonio, demand for small-bay and last-mile facilities remains solid. Otay Mesa in San Diego and West Phoenix are drawing serious interest from 3PLs and nearshoring occupiers despite macro headwinds like tariffs. Retail is proving remarkably resilient. Even with national closures, demand for quality space remains high—especially in high-income submarkets—fueling steady rent growth in San Diego, Phoenix, and Inland Empire.

Multifamily, meanwhile, faces its moment of digestion. A wave of new luxury units is colliding with affordability stress across markets, particularly in Phoenix (11.8% vacancy) and Las Vegas (9.6%). Concessions are widespread, and rent growth has turned negative in several metros. Still, absorption is healthy in markets like Fort Collins and San Diego, suggesting that demand exists—it just needs to catch up to supply. Office continues to struggle region-wide, with vacancy climbing past 16% in Phoenix and nearing record highs in Downtown San Diego. However, smaller, suburban spaces in places like Del Mar Heights and Chandler are still attracting tenants, reflecting a clear flight to quality and efficiency. Overall, Q1 signals not a market in freefall, but a sector in reset—clearing the runway for more strategic, sustainable growth ahead.

San Diego’s commercial real estate market in Q1 2025 presents varied conditions across the major property types—Office, Industrial, Multifamily, and Retail. This comprehensive review draws exclusively from CoStar’s detailed Q1 market reports to provide clarity and actionable insights for investors, property owners, brokers, and those new to commercial real estate.

As San Diego enters the second quarter of 2025, the commercial real estate (CRE) landscape reflects a bifurcated recovery. Some sectors are showing early signs of stabilization, while others struggle under the weight of high vacancies and economic stressors. Here’s a breakdown across the core sectors:

San Diego’s office market continues to face substantial headwinds, especially Downtown, where vacancies have reached unprecedented highs. The citywide vacancy rate stands at 12.9%, with Downtown alone facing a record-high availability above 35%, and industry insiders estimate true vacancy could be closer to 50%, factoring in unmarketed and underutilized space. Significant new developments like the completion of the 2.4M SF Campus at Horton and RaDD — with no tenants confirmed — intensifies the vacancy challenge.

The industrial market is experiencing mixed signals. Vacancy rates have climbed to 8.8%, a decade-high level driven by extensive new construction. The highest since 2013, due to 3.1M SF in new deliveries and over 2M SF in negative net absorption over the last 12 months. Otay Mesa is a bright spot, showcasing increased leasing activity driven by proximity to trade routes.

Multifamily properties are navigating a challenging environment characterized by substantial new unit deliveries, especially luxury units. Overall vacancy is stable at 5.0%, but submarkets like Downtown report vacancy rates exceeding 10%.

Retail remains relatively resilient with a 4.3% vacancy rate. Prime retail space remains scarce and in high demand, whereas older, lower-quality properties see longer vacancies.

San Diego’s commercial real estate landscape in early 2025 demands strategic adaptation. While office markets, especially Downtown, face structural challenges, industrial and retail sectors show selective strength, and multifamily grapples with high supply pressures.

Understanding these dynamics and responding strategically will be essential for success — whether you’re an investor, property owner, broker, or a newcomer.

Stay informed and proactive as the market continues to evolve.

Source: Costar

By SVN | Vanguard Commercial Real Estate Advisors, San Diego, CA

April 16, 2025

In this month’s economic update, we explore the shifting tides of small business sentiment, consumer behavior, real estate sectors, and employment data. Whether you’re an investor, developer, or just keeping a pulse on the market, here’s what you need to know to make informed, strategic decisions in Q2.

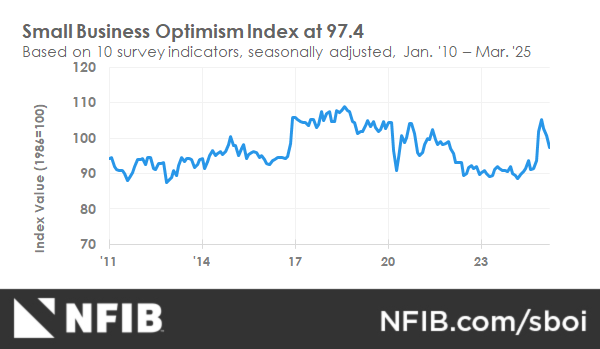

According to the National Federation of Independent Business (NFIB), small business optimism in March 2025 saw its sharpest monthly drop in nearly three years. Just 21% of business owners expect future conditions to improve, down significantly from February’s outlook. Only 3% anticipate increased sales in the short term.

Interestingly, the same business outlook components that surged following the November 2024 election have now reversed course, underscoring the volatile nature of political and economic sentiment.

What this means: Small businesses are approaching the next quarter cautiously. Expect scaled-back hiring, fewer expansion plans, and more risk-averse investment behavior across the board.

Morning Consult’s daily index shows consumer confidence experienced its second-largest three-day drop since the onset of the COVID-19 pandemic. After a post-election boost that carried into early 2025, consumer sentiment has been steadily declining.

While spending remained soft in February, forecasters anticipate a slight seasonal rebound due to the Easter holiday. Still, current trends suggest consumers are tightening their budgets in response to uncertainty around tariffs and broader inflation concerns.

The Logistics Managers’ Index (LMI) fell sharply from 62.8 in February to 57.1 in March, one of the steepest declines in its history. The drop is largely attributed to a cooldown in inventory costs, transportation prices, and warehouse demand—indicators that suggest the early-year rush to get ahead of tariffs has eased.

Although a reading above 50 still signals expansion, this downturn marks the shortest growth cycle in logistics in the past seven months.

Medical outpatient buildings (MOBs) are proving resilient in an otherwise cautious real estate environment. Asking rents increased 2.5% in 2024, and high-end properties led the way with stronger-than-average net operating income (NOI) growth.

With over 80% tenant retention rates and lease terms averaging nearly nine years, MOBs are drawing attention for their stability and long-term cash flow potential. Vacancy remains low at just 6.9%, further supporting investor confidence in this sector.

The National Multifamily Housing Council (NMHC) reports that 58% of developers are experiencing delays in Q1 2025—an improvement from the 78% figure at the end of 2024. Permitting remains the most common issue, followed by delays related to economic feasibility and professional services.

Geographically, the Southeast and Texas are facing more persistent slowdowns. While construction financing and labor shortages are improving, regulatory hurdles continue to test developer timelines.

The March jobs report from the Bureau of Labor Statistics delivered a surprise upside: 228,000 jobs were added, exceeding projections of 140,000. Healthcare and transportation led job growth, while the federal government continued trimming its workforce.

The unemployment rate ticked up slightly to 4.2%, but investor sentiment shifted toward a more dovish Federal Reserve stance. Markets are now forecasting a greater chance of multiple rate cuts by year-end.

Despite wavering confidence, the National Retail Federation predicts Easter 2025 spending will reach $23.6 billion, up from $22.4 billion in 2024. Discount stores are expected to capture the bulk of that spend, reinforcing the growing appeal of value-driven retail.

Egg prices, symbolic of seasonal inflation, have nearly doubled—yet Americans are still showing up to spend. Major retailers are optimistic, hoping to replicate December’s robust holiday sales performance.

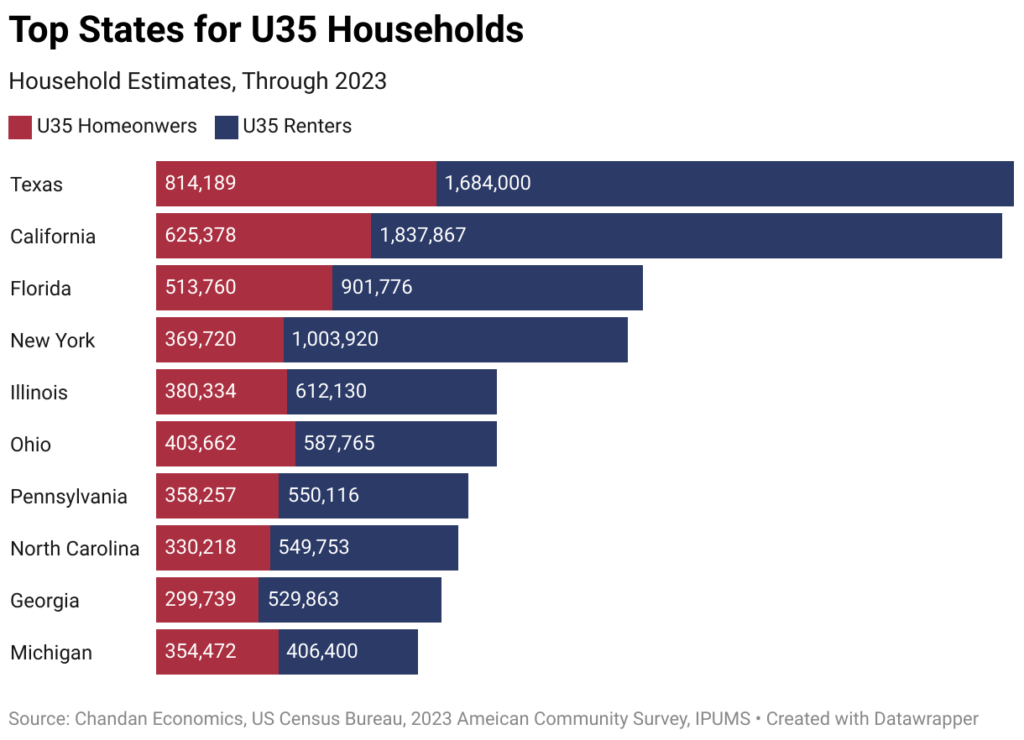

According to a recent analysis by Chandan Economics, Texas, California, and Florida lead the nation in the number of homeowners under age 35. However, when comparing under-35 homeowners as a percentage of all households, Utah, Alaska, and Iowa rank highest—signaling greater affordability.

In contrast, high-income states like California (4.6%), New York (4.8%), and Washington D.C. (3.5%) sit at the bottom, reflecting barriers to homeownership despite above-average wages.

The demand for work-from-home (WFH) rental units has dropped for the second consecutive year. There are now 4.0 million WFH rentals, down from a peak of 5.0 million in 2021. That’s a 20% decline over two years.

The market appears to be normalizing after the remote work surge of the pandemic. However, full-time remote workers are still 152% higher than pre-2020, suggesting long-term shifts remain in play.

The March Federal Open Market Committee (FOMC) meeting minutes reveal that the Fed chose to hold interest rates steady while assessing inflation and labor market signals. Policymakers acknowledged that inflation may run higher than expected due to new tariffs and supply chain pressures.

Most officials now see inflation risks as “tilted to the upside,” while risks to employment are growing on the downside.

While confidence may be shaky and geopolitical unknowns persist, not all sectors are retreating. Healthcare real estate, discount retail, and logistics remain areas of strength. In San Diego and beyond, this is a time to stay strategic—positioning ahead of rate cuts, leveraging tenant demand in core sectors, and anticipating changes in remote work trends.

Work Cited

SVN | Vanguard Commercial Real Estate Advisors.

Economic Update – April 10, 2025. SVN International Corp., 2025.

The 2025 SVN Annual Conference in San Antonio was an incredible experience, bringing together top commercial real estate professionals from across the country to collaborate, learn, and celebrate our shared success. Thanks to the SVN® International Corp. team for organizing an outstanding event filled with insightful speakers, networking opportunities, and industry-leading discussions.

Managing Directors: Pat Millay, Joe Bonin, & Cameron Irons

This year was especially momentous for SVN | Vanguard—after eight years of dedication and growth, we are proud to announce that we have been named the #1 SVN office in the United States! Out of more than 220+ offices nationwide, our team’s commitment to excellence, collaboration, and client success propelled us to the top.

Beyond our office’s success, we are thrilled to recognize the outstanding achievements of our top-performing Advisors.

Congratulations to our TEAM as well as the many other SVN | Vanguard Advisors who took home awards. Your hard work and dedication continue to set new standards in our industry.

Achieving the top ranking is a testament to the trust our clients place in us. At SVN | Vanguard, we don’t just close deals—we create long-term value for property owners, investors, and businesses across Southern California. Whether you’re looking to buy, sell, lease, or invest in commercial real estate, our team has the expertise, market knowledge, and nationwide network to help you achieve your goals.

Are you ready to work with the best? Contact SVN | Vanguard today and let’s discuss how we can maximize your real estate investments. Visit https://svnvanguard.com/ or call us at 619-442-9200 to get started.

Thank you again to SVN® International Corp. for an unforgettable conference, and congratulations to all the winners. Here’s to another year of growth, innovation, and success!

Southwest Region: 2024 Q2 Insights from SVN’s Regional Experts

If you’re wondering where the smart money is heading in commercial real estate, look no further than the Southwest Region. From the tech boom in San Diego to the resurgence of Las Vegas, and Denver’s growth spurt to the ever-evolving Los Angeles landscape, this region is buzzing with opportunity. But with so much happening, how do you separate the hype from the real deals?

That’s where our SVN Southwest Region team comes in. With boots on the ground in every key city—San Diego, Denver, Las Vegas, Los Angeles, Orange County, Inland Empire, Phoenix, Fort Collins, Albuquerque, Dallas Fort Worth, and Houston —we don’t just watch the market; we live it. Our local experts are quick in catching the latest trends, shifts, and opportunities before they hit the headlines. So, whether you’re an investor, developer, or just a real estate enthusiast, grab a cup of coffee (or maybe something stronger) and let’s dive into what’s happening right now in the Southwest Region commercial real estate market.

The Southwest Region: A Powerhouse of Diverse Real Estate Markets

Los Angeles and Orange County lead the way with their robust economies driven by tech, entertainment, and a resilient industrial sector. The tech and biotech industries continue to fuel growth in San Diego, while the Inland Empire keeps it position as a key logistics and distribution hub, powered by e-commerce. Meanwhile, Las Vegas is redefining itself beyond tourism and becoming a major player for innovation, logistics, and entertainment.

Heading east, we have Phoenix and Denver who are emerging as the top-tier choices for businesses and residents alike, thank to their competitive costs, lifestyle appeal, and growing job markets. Fort Collins, known for its high quality of life and emerging tech sector, complements the Denver market, while Albuquerque offer affordability and growth potential in market that is often overlooked.

Dallas-Fort Worth and Houston are both experiencing rapid growth, with DFW’s thriving corporate relocations and tech startups, while Houston has its diversified economy and its strong industrial / office demand.

As these cities continue to evolve, the Southwest Region presents an abundance of opportunities with each market offering a unique dynamic and potential for growth. It’s a region where staying ahead means staying informed , and any of our SVN® teams are here to provide you with the best advice and market information you need to navigate the commercial real estate world.